The ongoing conflict in the Middle East has created a ripple effect across the global economy. The rising cost of energy is shaking up almost every type of investment. While these swings feel intense, it is important to remember that this is likely a short-term reaction to geopolitical events rather than the end of the long-term growth trend we’ve been seeing in the markets.

The current market dynamic: A breakdown in tradition

Historically, during times of war, investors flock to “safe havens.” However, the current correlation breakdown has made traditional hedging difficult:

- Broken safe havens: Both Gold and Government Bonds have faced selling pressure, with yields rising despite the uncertainty.

- The dollar as a redoubt: The U.S. Dollar remains one of the few effective hedges currently functioning in the market.

- The oil catalyst: Oil is the primary transmission mechanism of this crisis. If prices remain elevated, the resulting “energy shock” could compound existing inflation, potentially forcing central banks into a policy mistake by tightening too aggressively into a slowing economy.

Our base case: A correction, not a collapse

We believe we are experiencing a short-term correction within a long-term bull market. While the path forward remains clouded by the situation in Iran, several indicators suggest a bottom may be near.

- Valuation and earnings

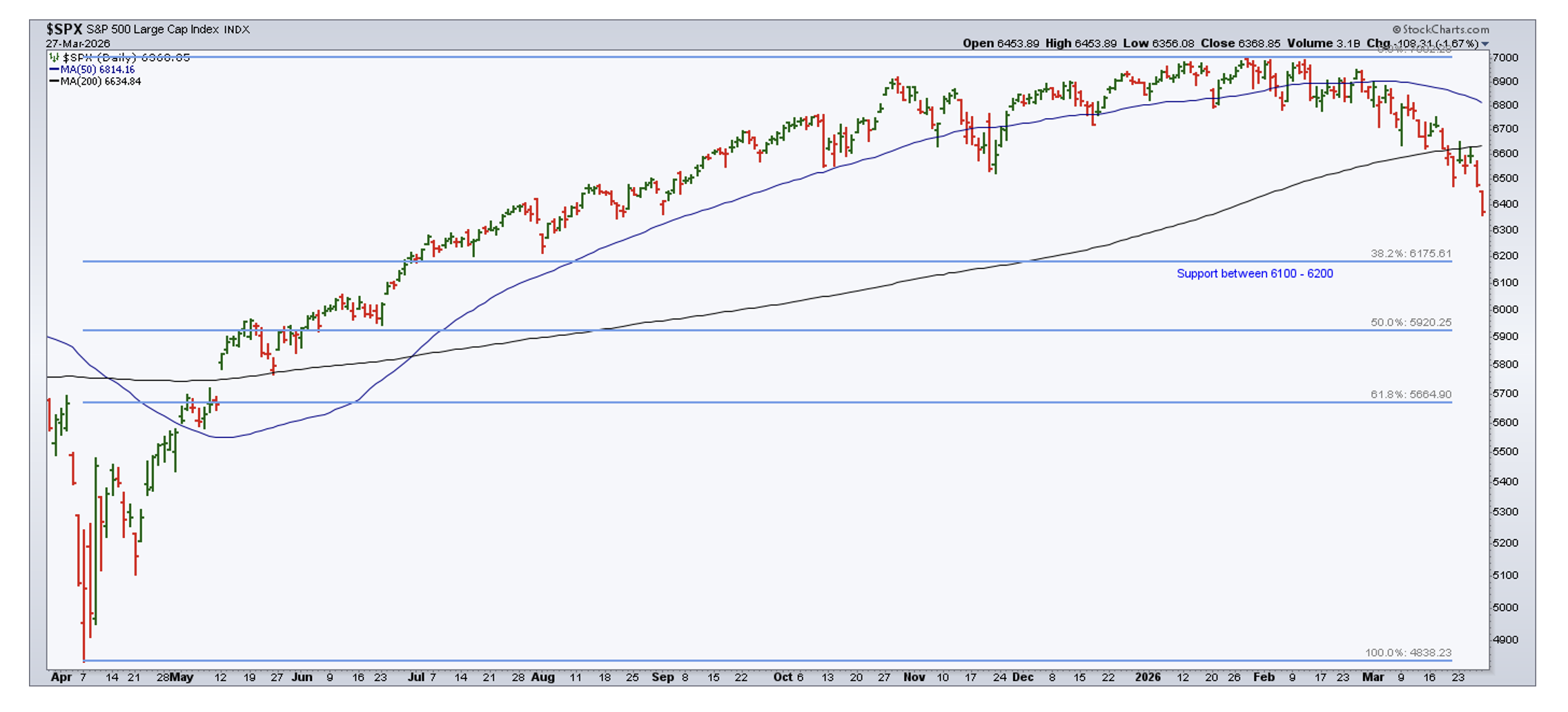

The S&P 500 P/E ratio has compressed from over 22x at the start of the year to below 20x based on 12-month forward estimates. Crucially, this de-risking has occurred while expected earnings growth has actually increased, creating a more attractive entry point for disciplined investors. Technical support levels

With the market recently breaking below its 200-day moving average, we are watching two key technical “floors” where we expect buyers to step in:- Primary support (~6175): This aligns with the 38% Fibonacci retracement level, suggesting a potential further 3% downside before a firm bottom.

- Secondary support (~5920): A logical secondary floor should the initial level fail to hold.

The path to recovery vs. the “bear” case

The trajectory of the market depends heavily on the stabilization of energy prices and the status of global shipping lanes.

| The bull catalyst (recovery) | The risk catalyst (recession) |

| Resolution of conflict in Iran leads to oil returning to the $70/bbl range. | Oil spikes above $150/bbl, causing a massive demand shock. |

| Reopening of the Straits within the expected one-month window. | Prolonged closure of the Straits, leading to stagflation. |

| Markets follow historical patterns of rapid recovery post-energy shocks. | The Fed is forced to keep rates “higher for longer” due to energy-led inflation. |

Strategic summary

Energy prices are the primary driver of recent market volatility, and the market may not be fully pricing in the risk of a long-term closure of the Straits. But if the tension eases in the next few weeks as expected, the downward pressure on stocks and upward pressure on yields should stabilize alongside oil.

Our outlook

We remain constructive. While we anticipate the market could experience more volatility as it searches for a definitive floor, the combination of lower valuations and resilient earnings growth suggests the long-term upward trend is still intact.

Final thought

Volatility is the price of admission for long-term gains. By staying disciplined and focused on fundamentals, we believe investors can weather this correction and benefit from the eventual stabilization of the global landscape.

IMPORTANT DISCLOSURE

The statements made in this newsletter are, to the best of our ability and knowledge, accurate as of the date they were originally made. But due to various factors, including changing market conditions and/or applicable laws, the content may in the future no longer be reflective of current opinions or positions.

Any forward-looking statements, information and opinions including descriptions of anticipated market changes and expectations of future activity contained in this newsletter are based upon reasonable estimates and assumptions. However, they are inherently uncertain and actual events or results may differ materially from those reflected in the newsletter.

Nothing in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice. Please remember to contact Signet Financial Management, LLC, if there are any changes in your personal or financial situation or investment objectives for the purpose of reviewing our previous recommendations and/or services. No portion of the newsletter content should be construed as legal, tax, or accounting advice. The views and opinions expressed in this report are solely those of the author and should not be attributed to Summit Financial, LLC., a SEC Registered Investment Adviser.